![]() Call us now:

Call us now:

Employee taxation in Thailand

Thailand offers a vibrant culture, breathtaking landscapes, and a dynamic economy, which makes the country an attractive destination for business and employment. However, employers and employees who conduct business in Thailand must understand the tax system to avoid legal violations and financial penalties. As global business activities expand, employee taxation in Thailand has become an increasingly important issue to address.

Table of Contents

What are the regulations concerning employee taxation in Thailand ?

There are several regulations governing employee taxation in Thailand:

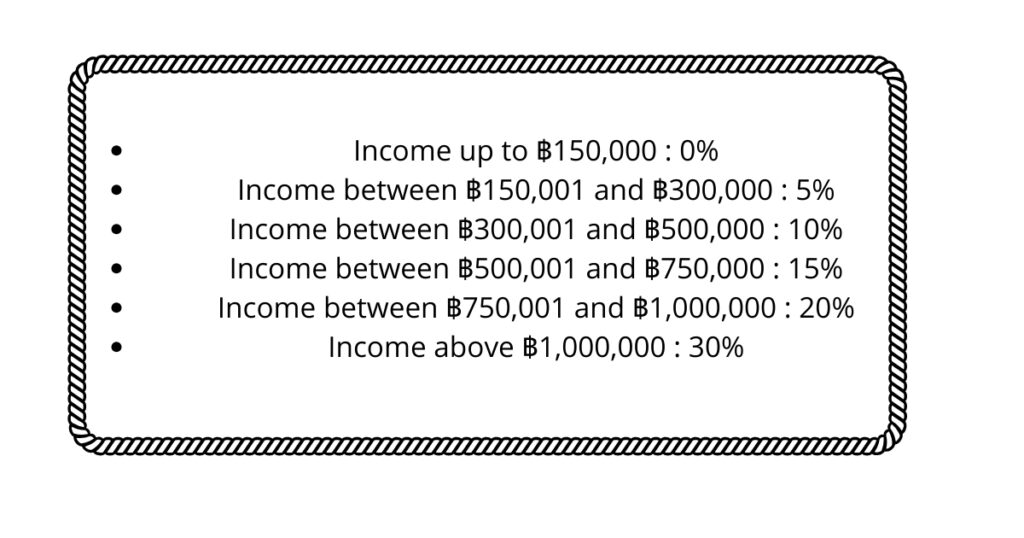

Personal Income Tax (PIT)

Thailand taxes residents on their worldwide income under Personal Income Tax (PIT), while it taxes non-residents only on income sourced in Thailand. The tax system applies progressive rates ranging from 0% to 35%, depending on the income bracket.

Employers must withhold the applicable tax from employees’ monthly salaries and remit it to the Revenue Department. Employees must also file an annual personal income tax return to reconcile the total tax withheld and claim any applicable refunds.

Tax Deductions and Allowances

Employees may claim various deductions and allowances to reduce taxable income. These include deductions for healthcare expenses, education expenses, contributions to provident funds, and social security contributions. The law also grants additional allowances for dependents, disabled dependents, and certain qualifying investments.

Social Security Contributions

Thailand operates a compulsory social security system for both employers and employees under the Social Security Act B.E. 2533 (1990). The system provides benefits such as medical care, maternity benefits, disability compensation, and old-age pensions. Employers deduct contributions proportionally from employees’ monthly wages, subject to a statutory maximum threshold.

Tax Treaties

Thailand has concluded double taxation treaties with several countries to prevent double taxation and reduce the tax burden for foreign employees. These treaties define the taxation rights of each contracting state. In certain cases, non-resident employees may qualify for exemption from Thai taxation if they meet specific conditions regarding duration of stay and source of income.

Compliance and Reporting

Employers must prepare and submit employee income withholding forms (such as Form PND.1) to the Revenue Department and provide the relevant statements to employees. Employees must file their annual income tax return (Form PND.90 or PND.91, as applicable) to report total income and calculate their final tax liability.

What Law Applies?

The Revenue Code of Thailand serves as the principal law governing employee taxation in Thailand. It establishes the legal framework for assessing, calculating, and collecting personal income tax. The Code regulates the determination of taxable income, applicable tax rates and brackets, allowable deductions, and available allowances. It also defines the duties and responsibilities of employers and employees regarding income tax withholding and remittance to the tax authority.

In addition to the Revenue Code, other laws and regulations may govern specific aspects of employee taxation. For example, the Social Security Act B.E. 2533 (1990) regulates the social security system and mandatory contributions. Double taxation treaties between Thailand and other countries allocate taxing rights and provide guidance on the taxation of foreign employees.

Employers, employees, and tax professionals must comply with the Revenue Code, related legislation, official tax notifications, and circulars issued by the Revenue Department of Thailand.

Get expert legal guidance.

How Is Employee Tax Calculated?

Thailand calculates employee income tax, specifically Personal Income Tax (PIT), under a progressive tax rate system in accordance with the Revenue Code of Thailand. The calculation follows these steps:

1. Determine Taxable Income

First, calculate the employee’s total income, including salary, bonuses, allowances, benefits-in-kind, and other taxable earnings. Then apply all eligible deductions and allowances, such as those for education expenses, healthcare expenses, provident fund contributions, and social security contributions. After subtracting these amounts, the remaining figure constitutes the taxable income.

2. Identify the Applicable Tax Bracket

Thailand divides personal income into progressive tax brackets, with higher rates applying to higher income levels. The tax rates currently range from 0% to 35%, depending on the income band. Each portion of income falls into a specific bracket and is taxed at the corresponding rate.

3. Apply Progressive Tax Rates

Calculate the tax liability by applying the relevant tax rate to each portion of income within the applicable tax bracket. For example, if part of an employee’s taxable income falls within the 15% bracket, apply the 15% rate only to that portion of income.

4. Apply Tax Allowances and Credits

After calculating the initial tax liability under the progressive rate system, apply any additional tax allowances and credits that reduce the overall tax burden. These may include allowances for dependents, disabilities, long-term equity fund investments, and other qualifying items.

5. Withholding and Payment

Employers must calculate and withhold income tax from employees’ monthly salaries in accordance with the Revenue Code of Thailand. Employers must then remit the withheld amount to the Revenue Department within the prescribed deadlines. If the employee’s total annual tax liability exceeds the amount withheld, the employee must pay the outstanding balance.

Because tax rates and income thresholds may change, employers and employees should consult the latest guidance issued by the Revenue Department of Thailand or seek professional tax advice to ensure accurate tax calculation and compliance.

Conclusion

Thailand governs employee taxation through a structured and comprehensive legal framework that promotes fairness, transparency, and compliance. The Revenue Code of Thailand forms the cornerstone of this system and regulates the assessment, calculation, withholding, and payment of Personal Income Tax (PIT).

Thailand applies a progressive tax rate system under which tax rates range from 0% to 35%, depending on taxable income levels. Employers play a central role in ensuring compliance because they must withhold tax from employees’ salaries and remit it to the Revenue Department. Employees must file annual tax returns to reconcile withheld amounts and claim applicable deductions or refunds.

In addition to personal income tax, the Social Security Act B.E. 2533 (1990) requires mandatory social security contributions as part of the overall employee taxation framework. International employees may also benefit from double taxation agreements that Thailand has concluded with other countries.

If you need further information, you may schedule an appointment with one of our lawyers.

Employee taxation is primarily governed by the Revenue Code of Thailand, which sets out rules on taxable income, tax rates, deductions, withholding obligations, and filing requirements.

Thai tax residents are taxed on their worldwide income, while non-residents are taxed only on income derived from sources within Thailand.

Thailand applies progressive tax rates ranging from 0% to 35%, depending on the employee’s taxable income bracket.

Yes. Employers must withhold personal income tax from employees’ monthly salaries and remit it to the Revenue Department. They must also issue the relevant tax forms to employees for annual filing purposes.

Yes. Employees are generally required to file an annual personal income tax return (Form PND.90 or PND.91) to reconcile total income, claim deductions and allowances, and determine whether additional tax is payable or a refund is due.